-

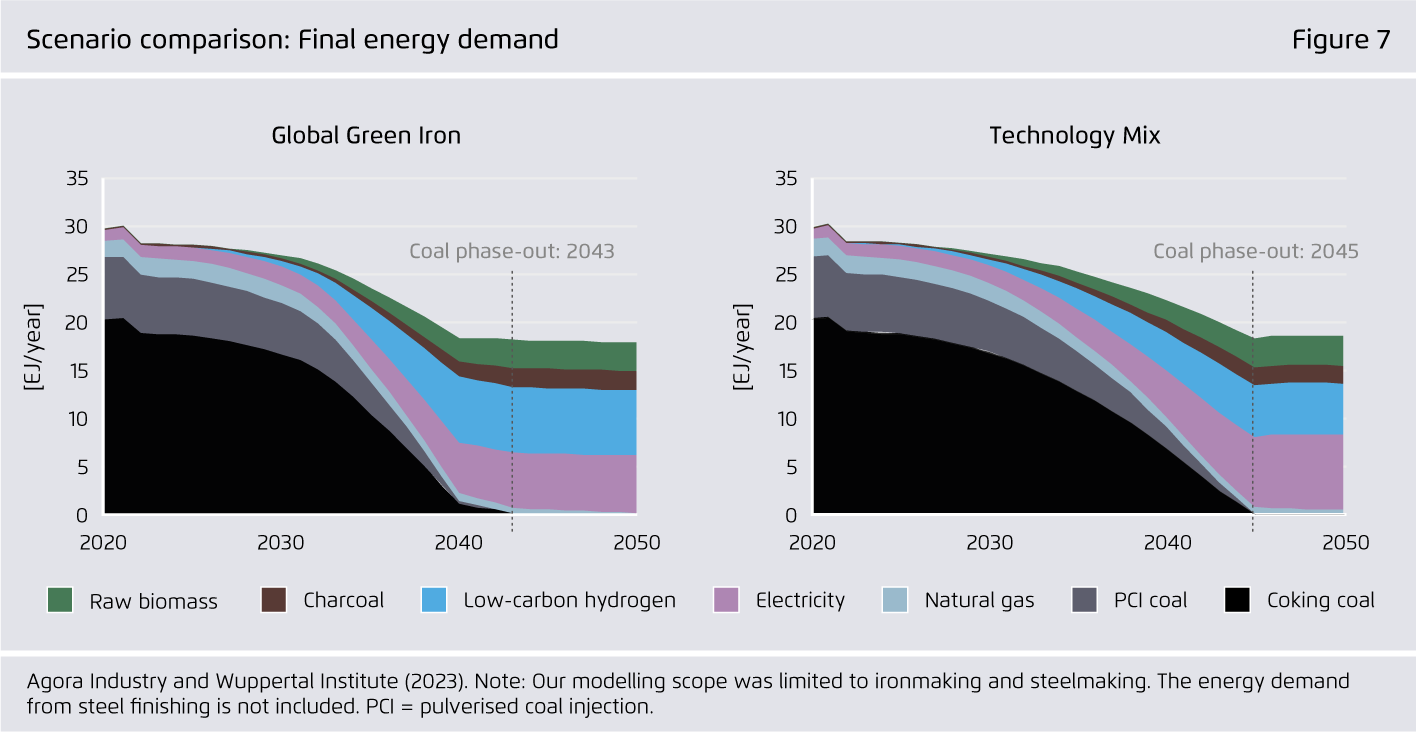

A net-zero steel sector and a coal phase-out in steelmaking by the early 2040s are technically feasible. This can turn iron and steel from a hard-to-abate to a fast-to-abate sector and be a key element to increase global climate ambition.

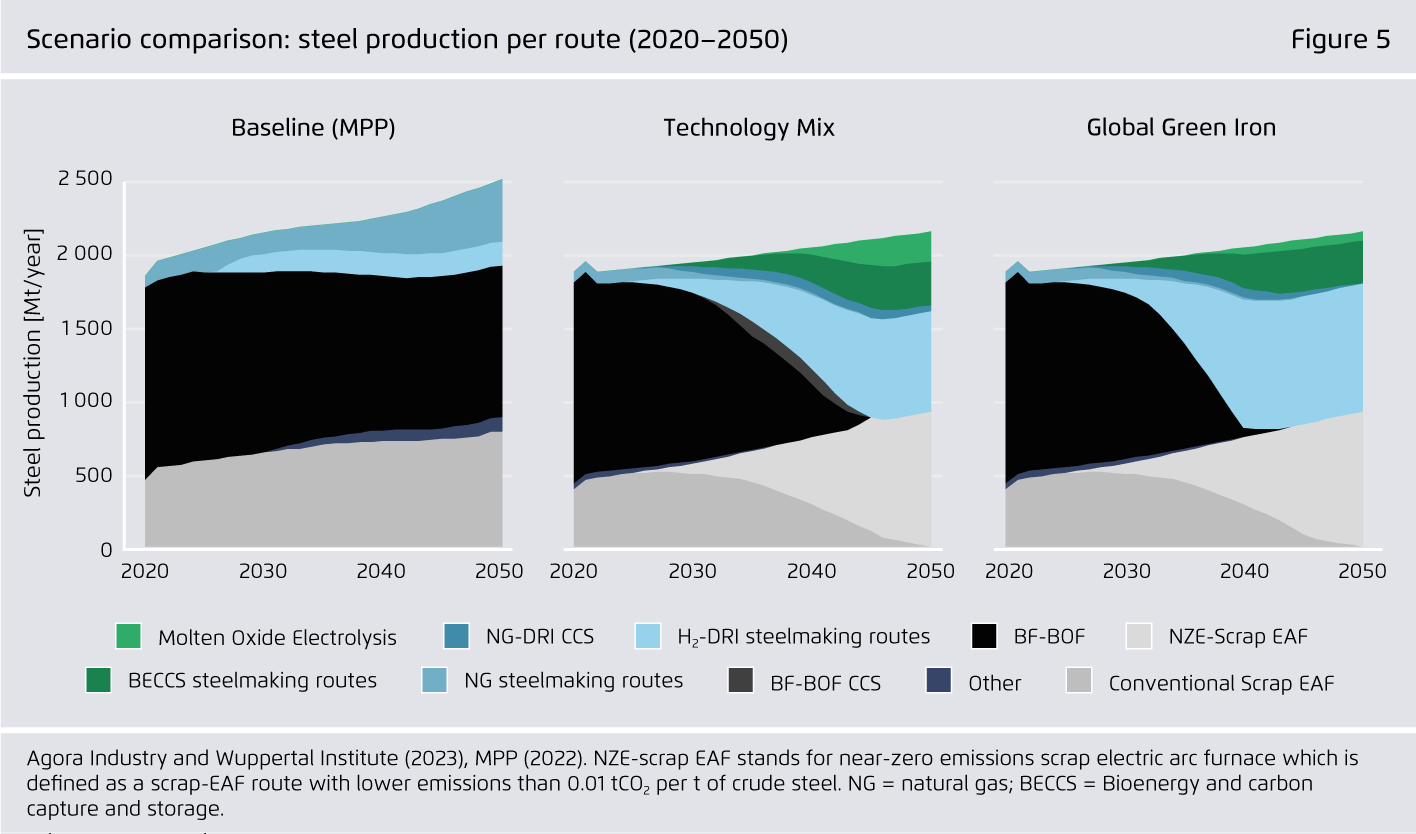

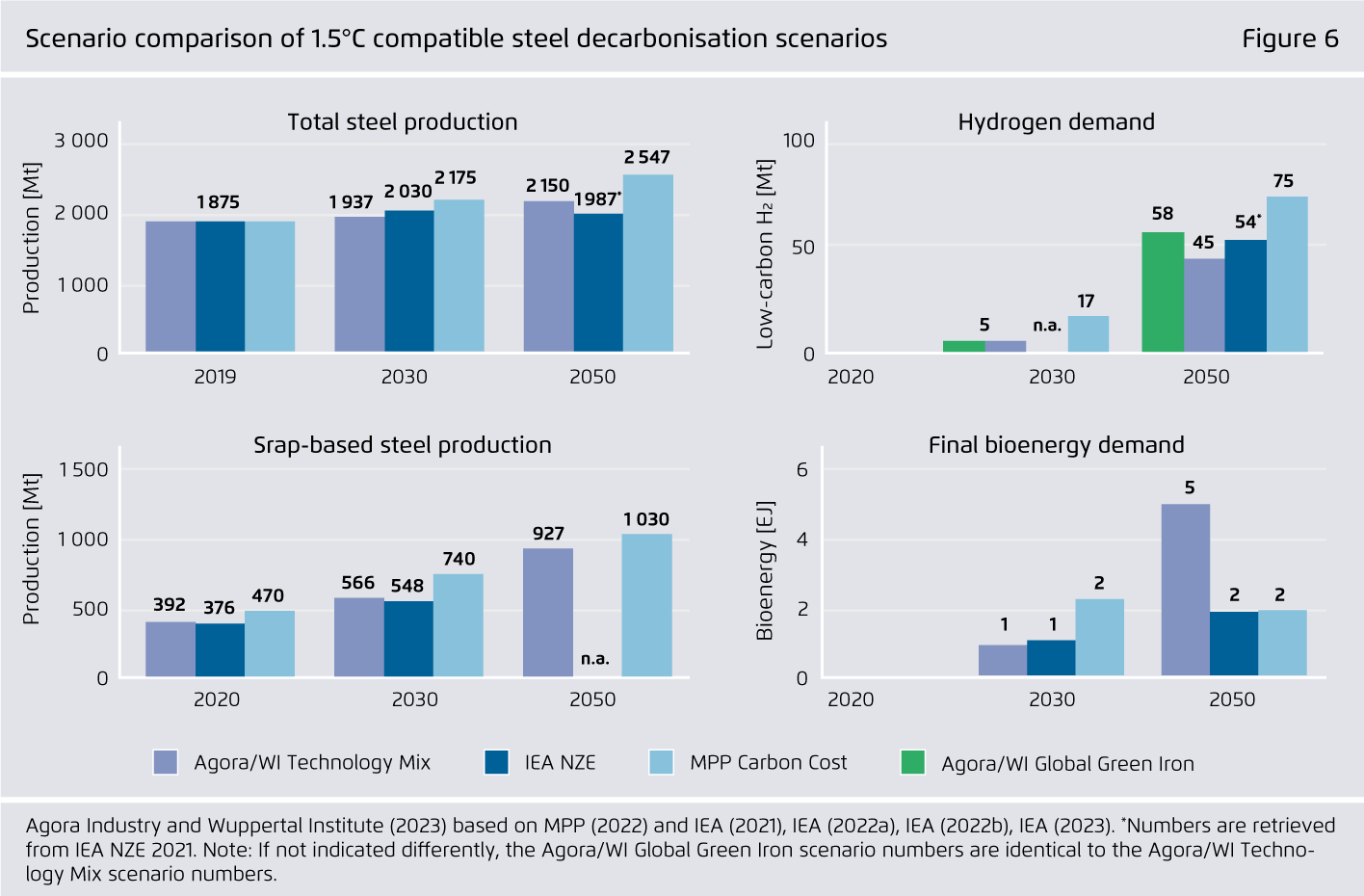

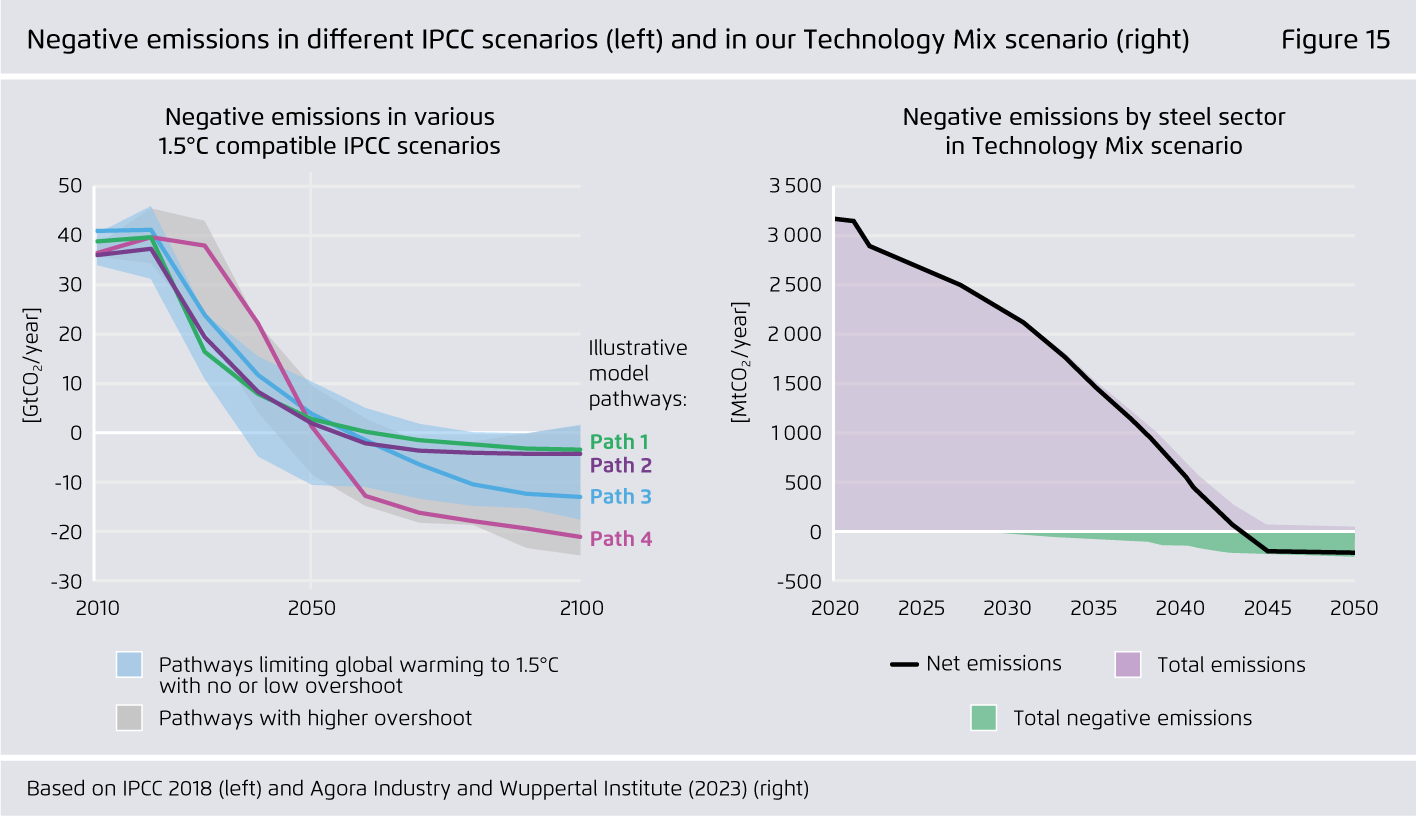

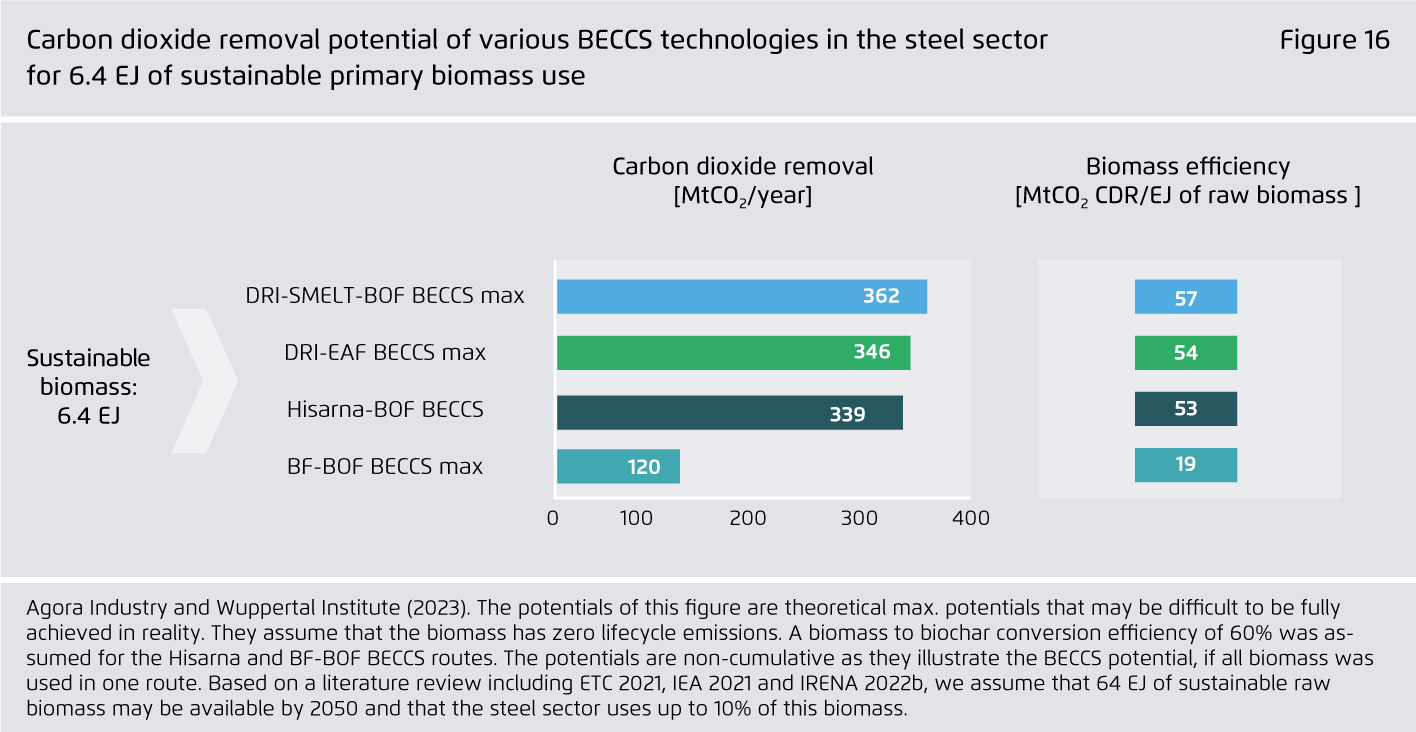

The key strategies to achieve such an accelerated steel transformation are material efficiency, an increase of scrap- and hydrogen-based steelmaking plus bioenergy and carbon capture and storage (BECCS).

-

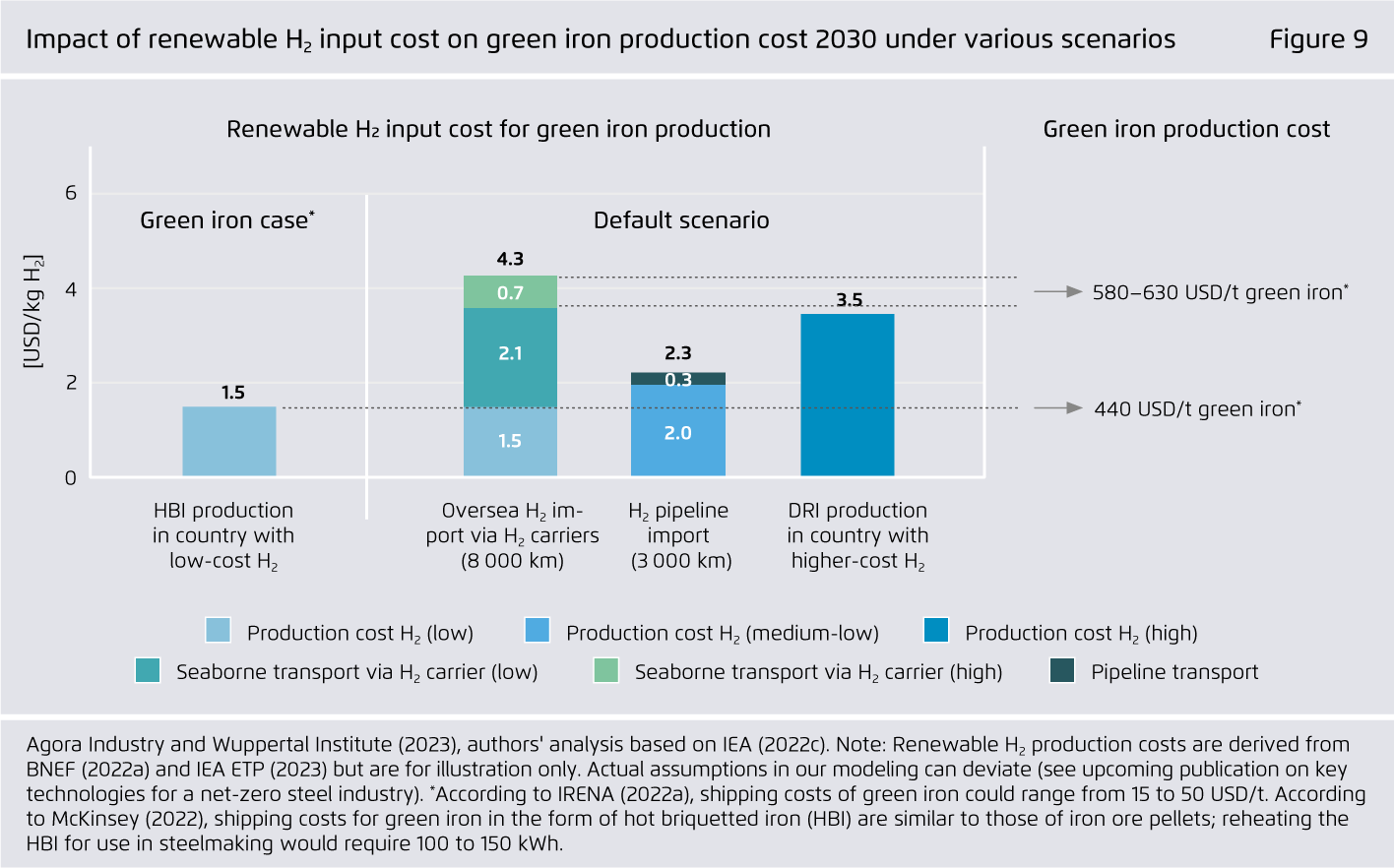

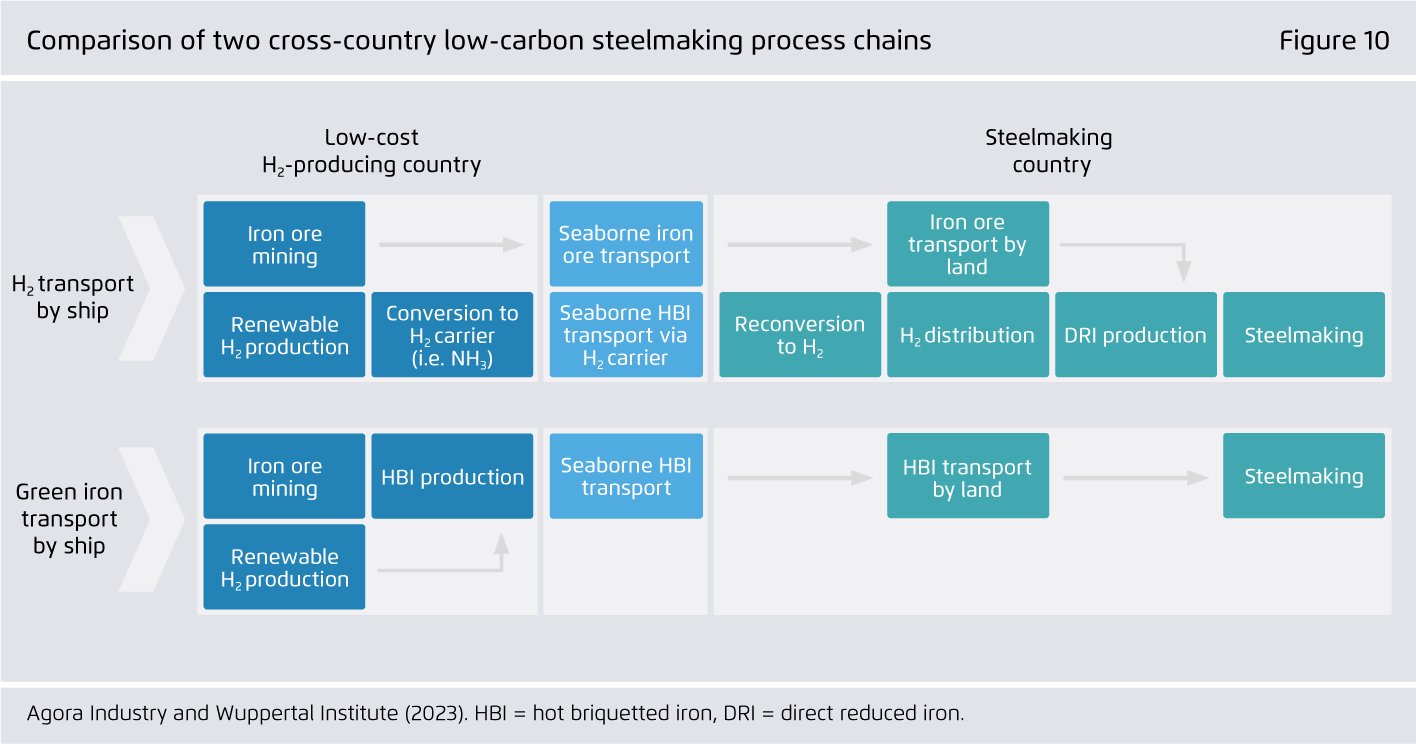

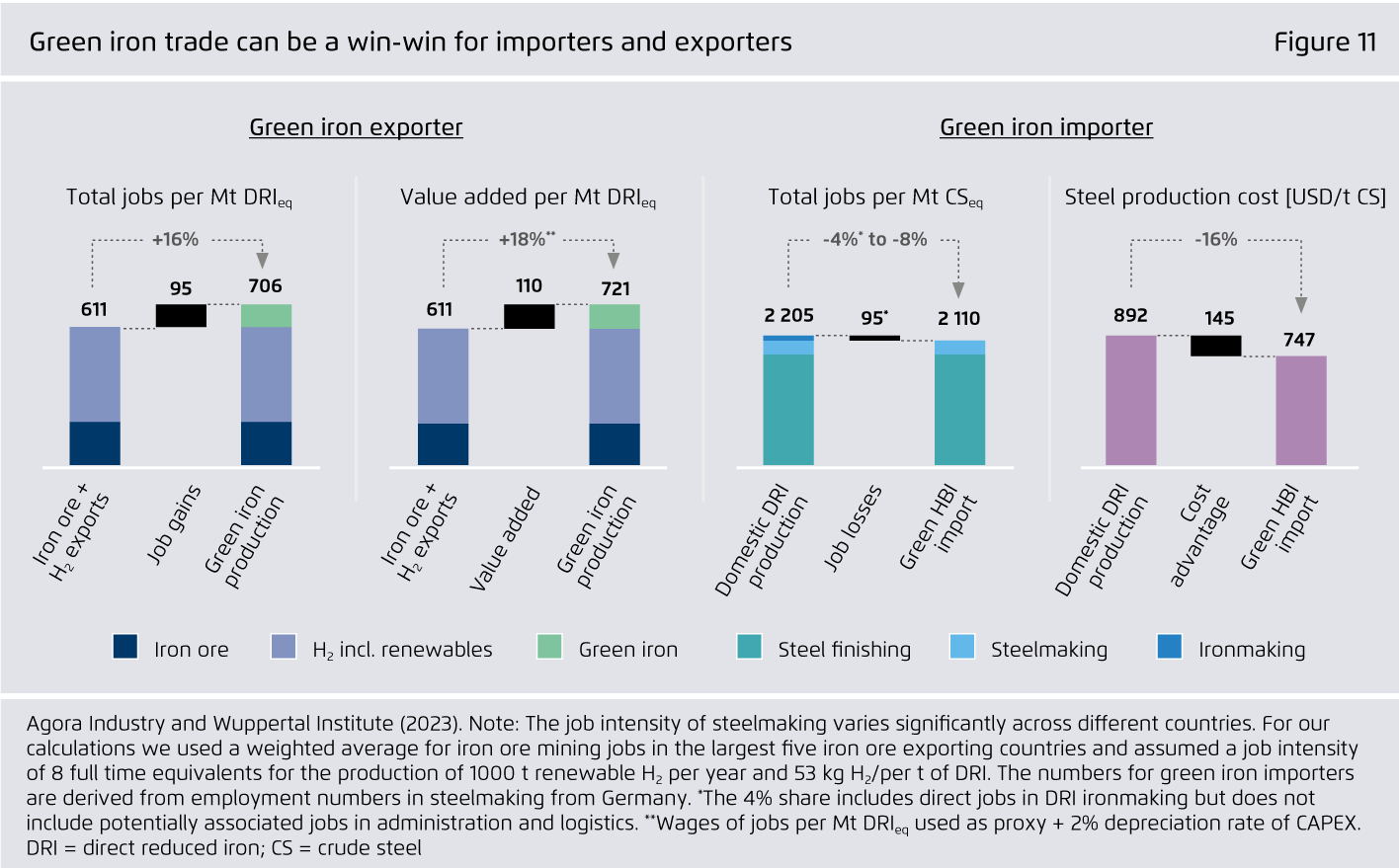

Green iron trade can lower the costs of the global steel transformation and can be a win–win solution for green iron exporters and importers.

Transporting embodied hydrogen (H₂) as green iron will be significantly cheaper than transporting H₂ and its derivatives by ship. For countries with high renewable H₂ costs, green iron imports can increase the competitiveness of low-carbon steelmaking, thereby helping to safeguard local jobs in the steel industry. For green iron exporters, this can create new jobs and value added.

-

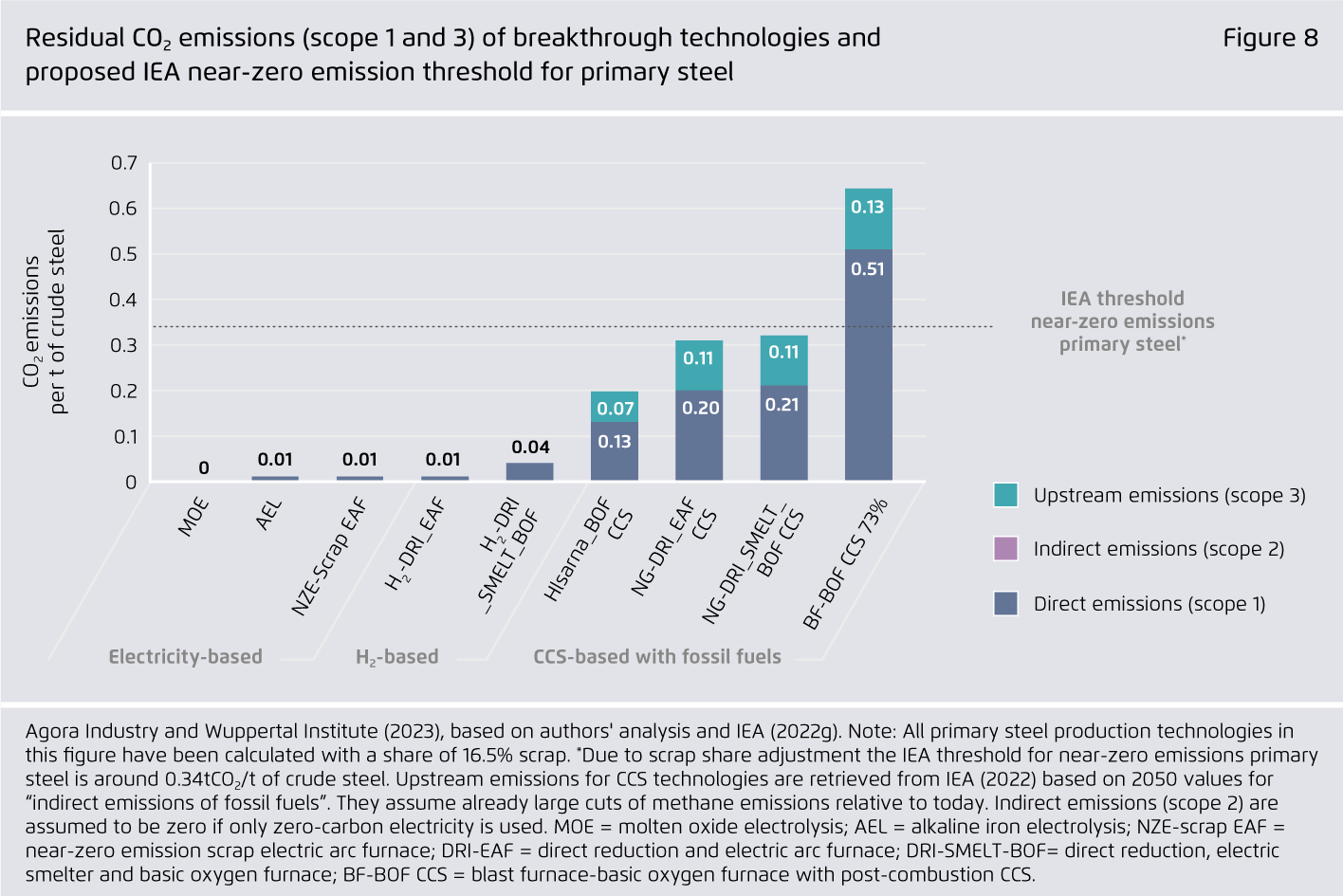

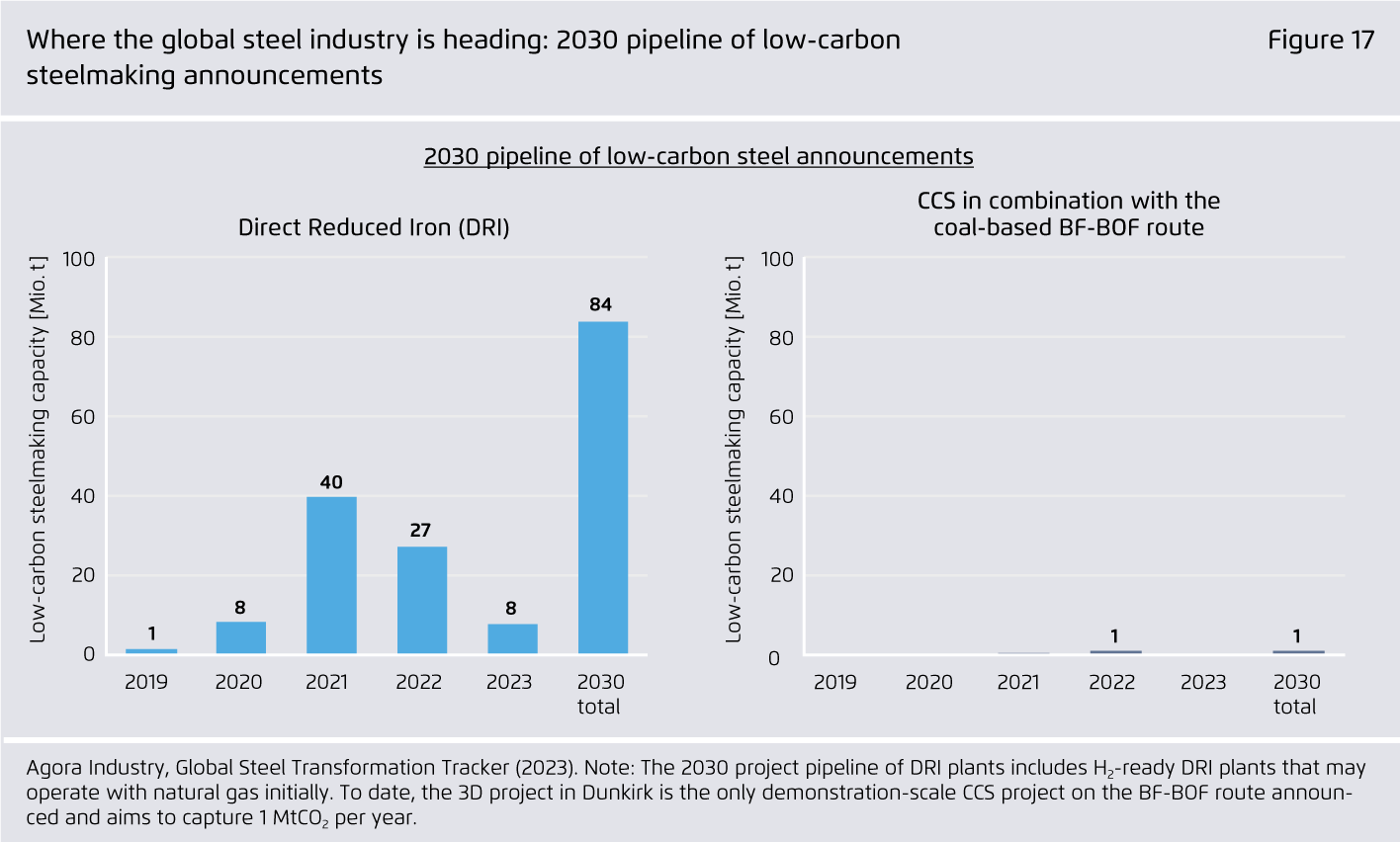

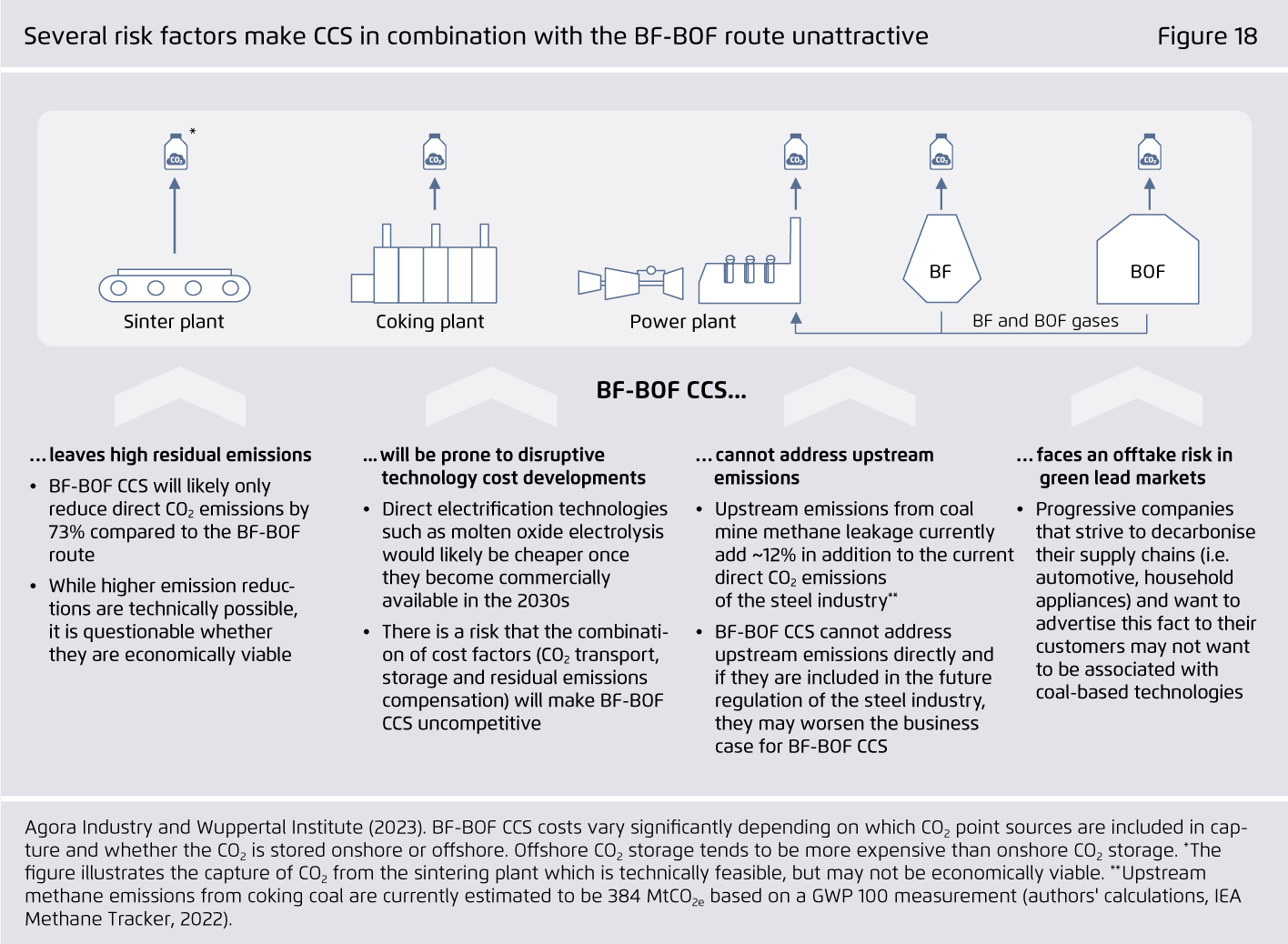

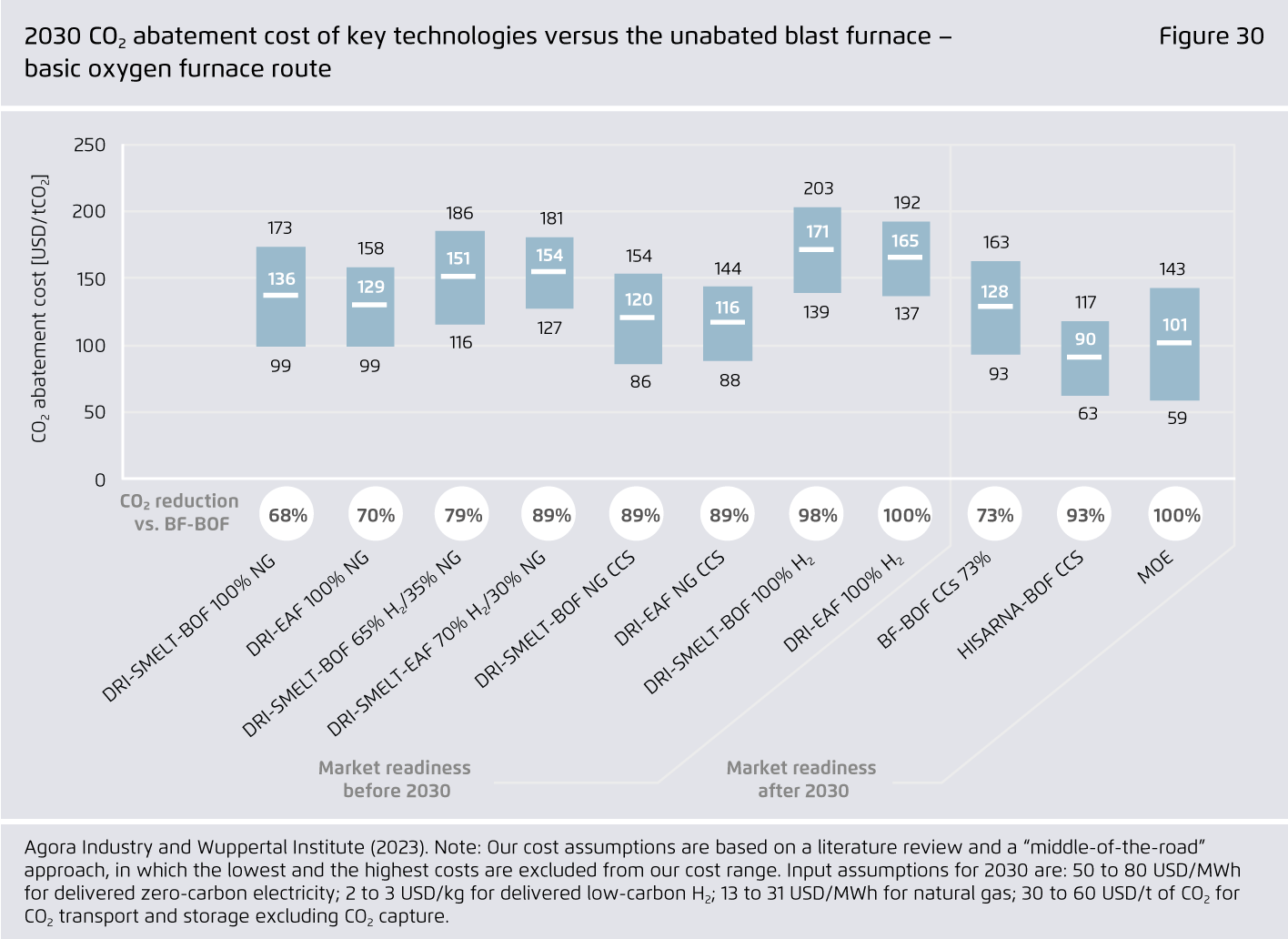

Carbon capture and storage (CCS) on the coal-based blast furnace-basic oxygen furnace route (BF-BOF) will not play an important role in the global steel transformation.

CCS on the BF-BOF route is unlikely to reduce direct CO₂ emissions beyond 73% and cannot address upstream emissions (coal mine methane leakage). Compared to other key technologies, steelmakers’ efforts to commercialise this technology are currently very low. If BF-BOF CCS does not materialise, new coal-based steel plants face a high carbon lock-in and stranded asset risk.

-

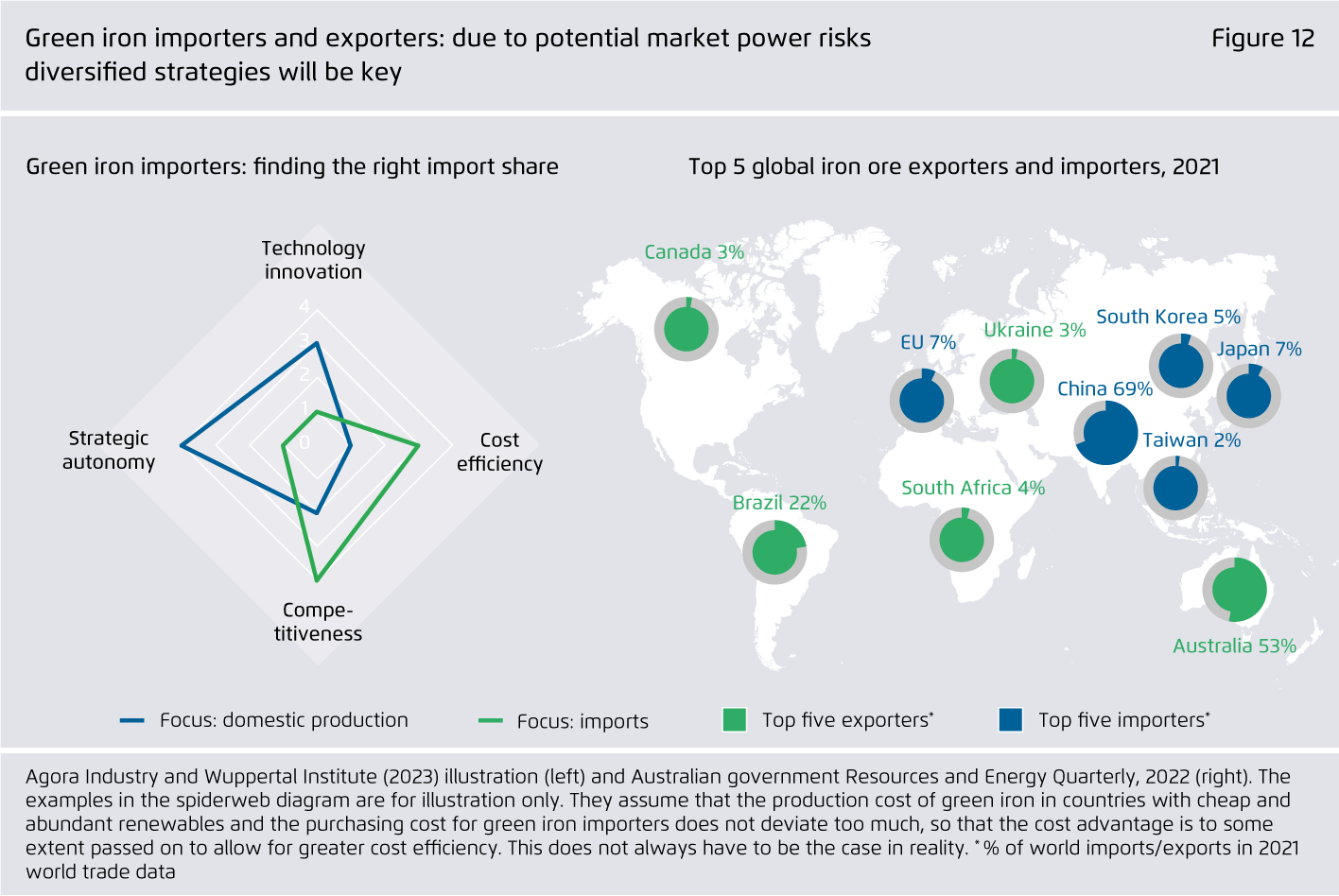

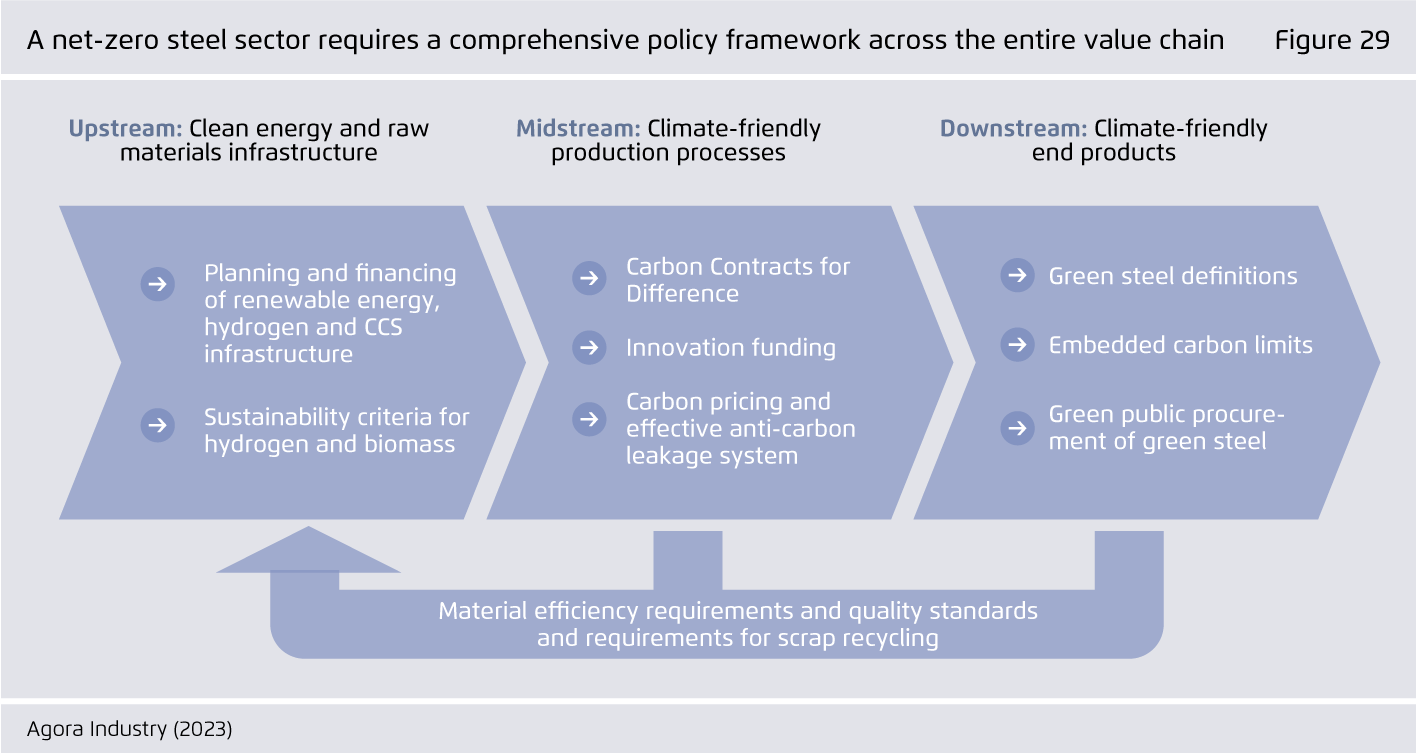

To unlock the full acceleration potential of the steel transformation, national governments need to create an adequate regulatory framework and develop cross-country strategic partnerships.

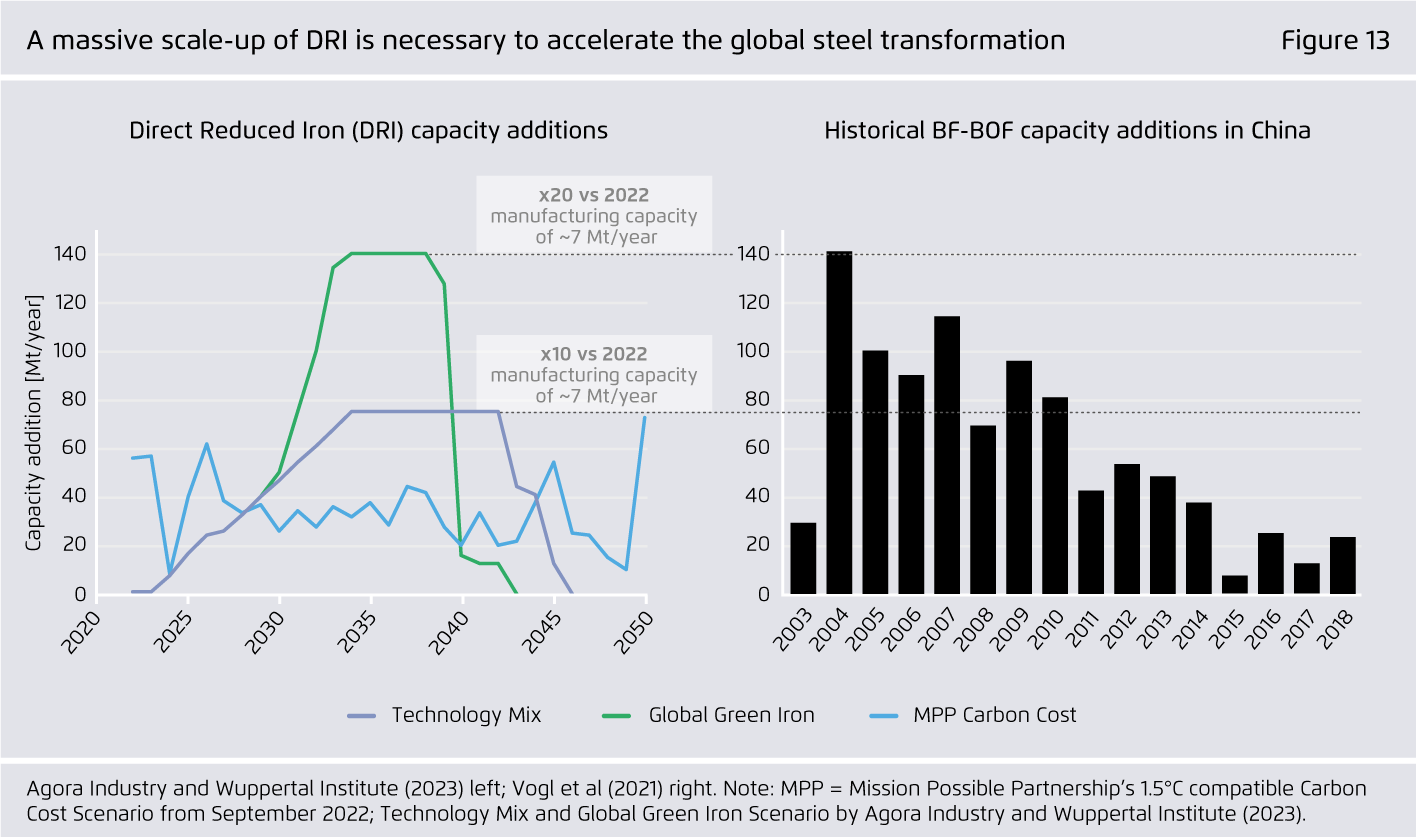

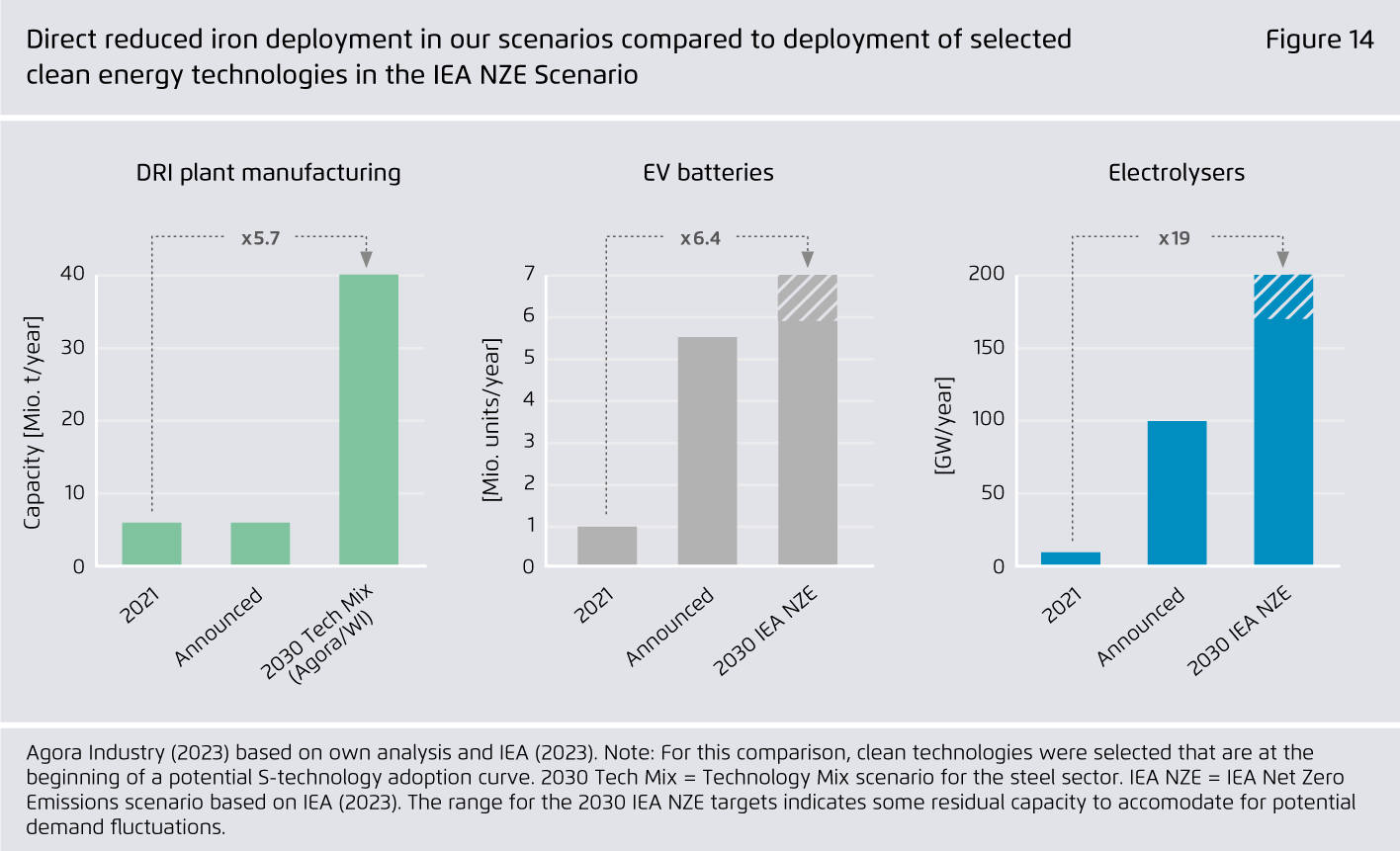

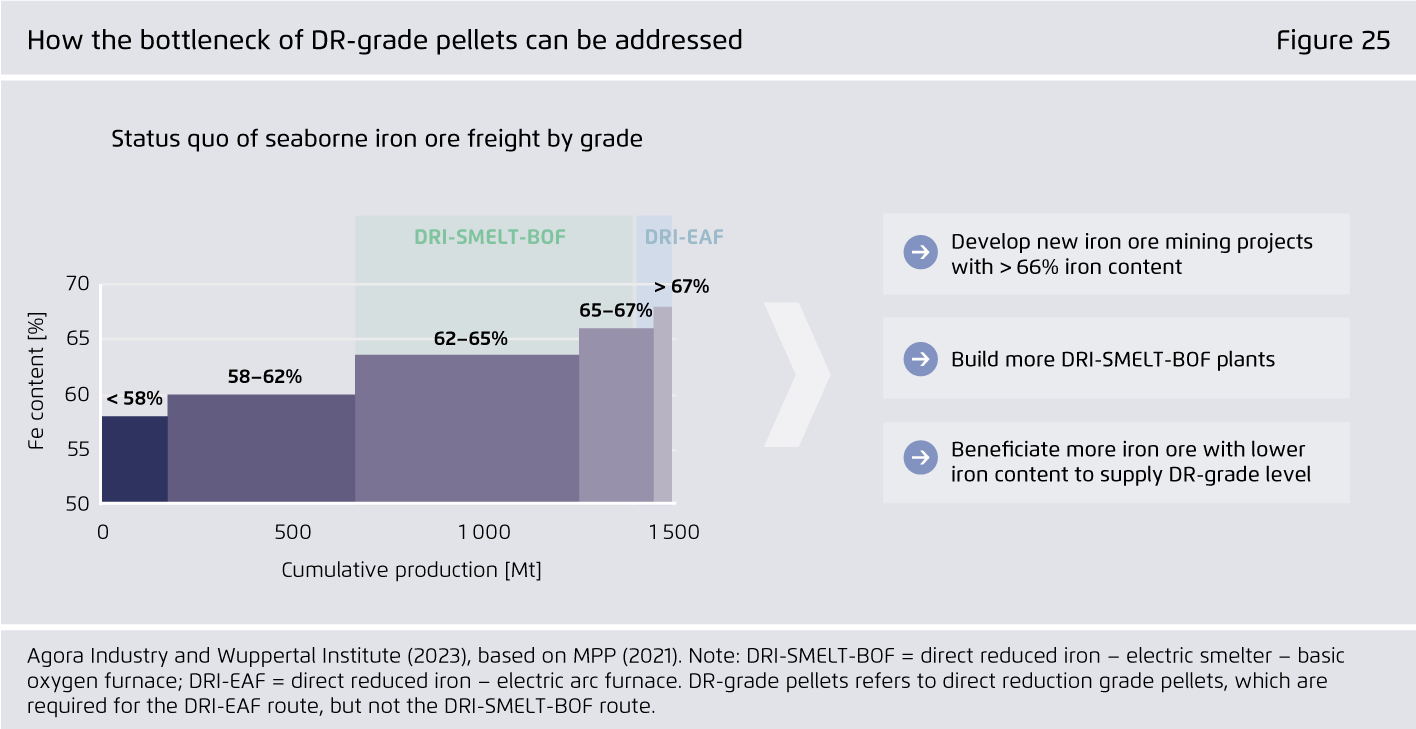

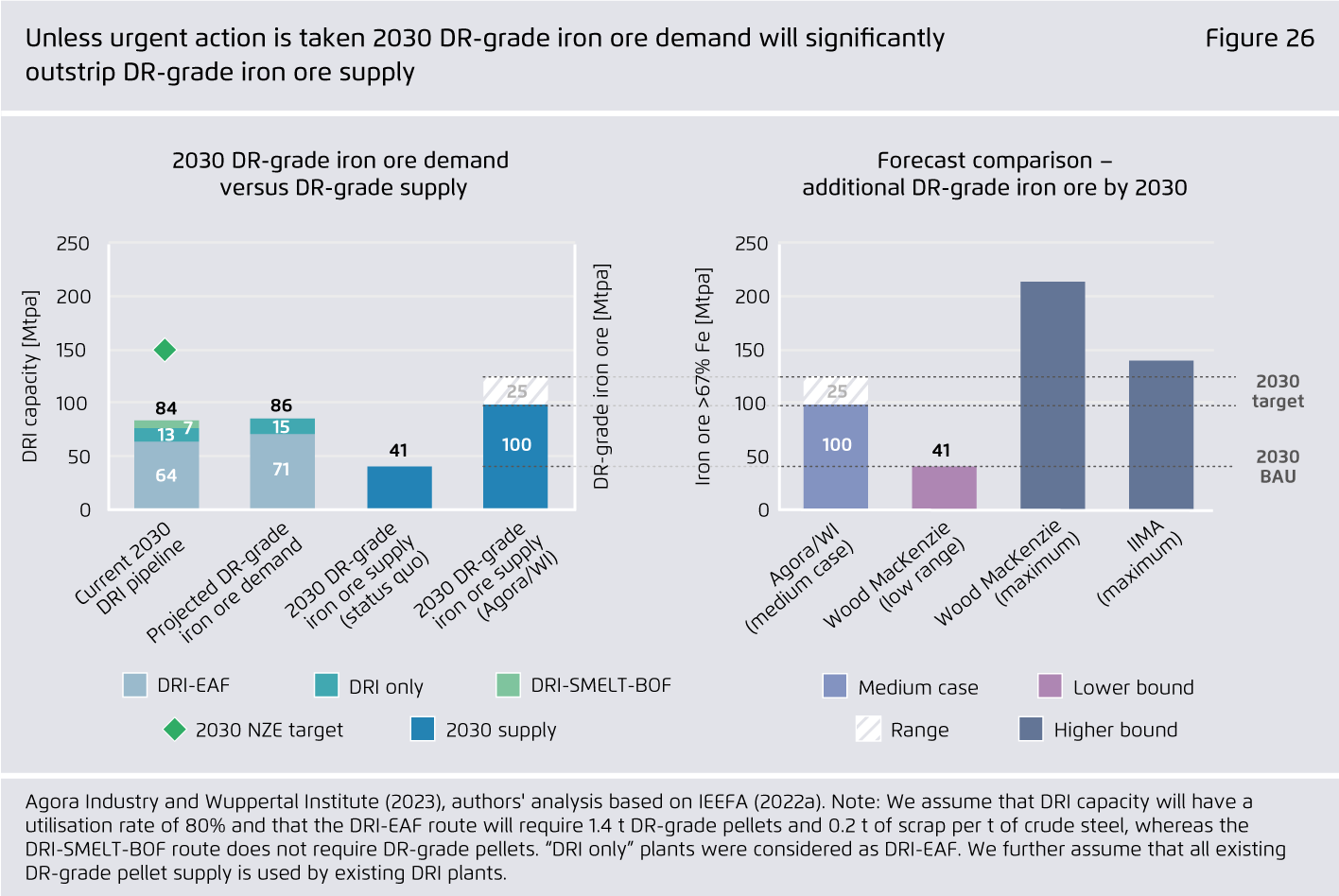

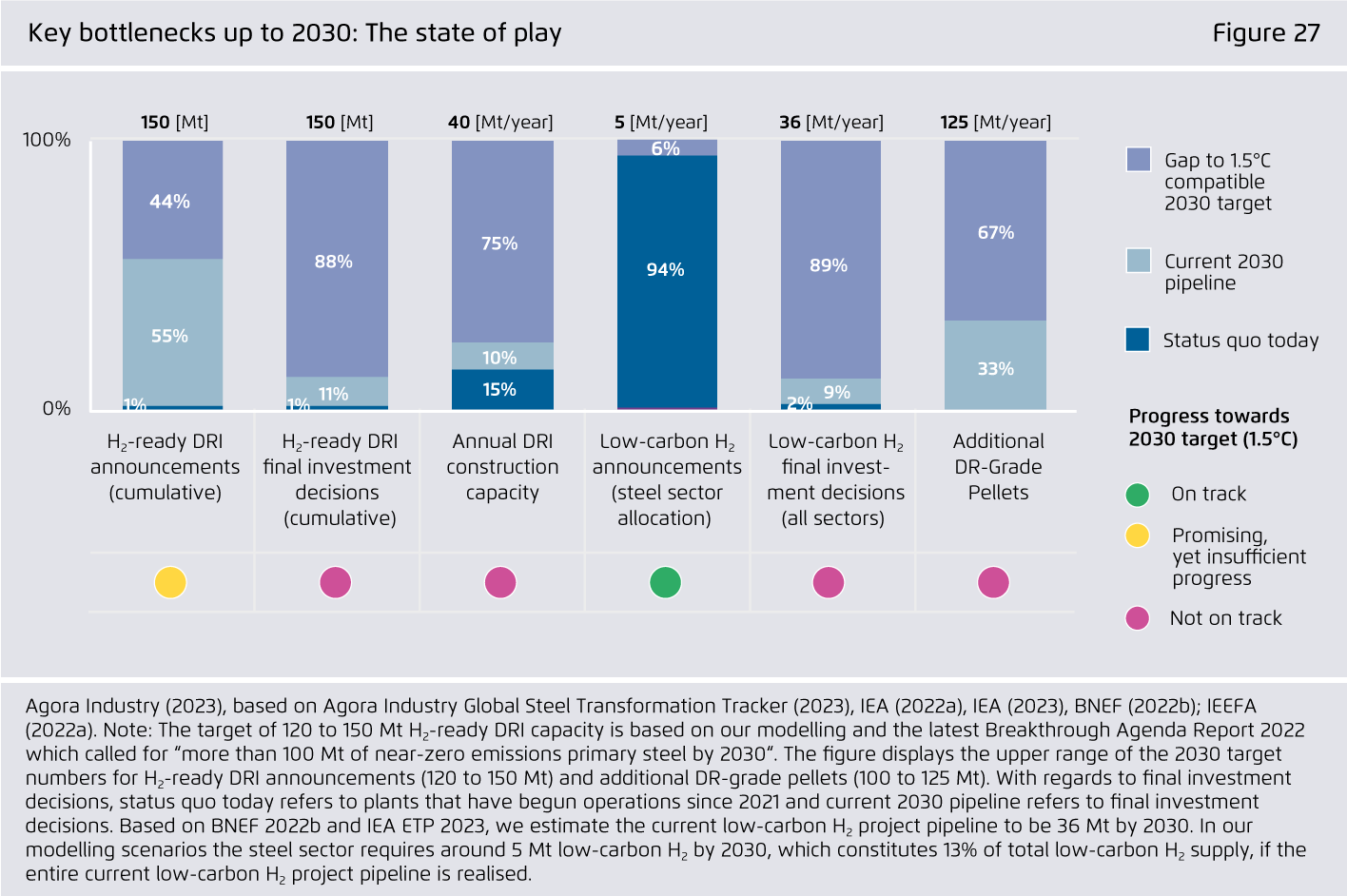

International cooperation will be needed to address key bottlenecks (i.e. DRI plant engineering, suitable iron ore qualities, low-carbon H₂), minimise stranded assets and help to unlock green iron trade.

15 insights on the global steel transformation

This study summarises the key findings of our work on the global steel sector.

Preface

“We are walking when we should be sprinting.” With these words the Intergovernmental Panel on Climate Change (IPCC) Chair Hoesung Lee summed up the latest IPCC Synthesis Report. This IPCC report estimates that with currently implemented policies, the world is projected to warm by 3.2°C by 2100. Much greater efforts are needed to drive down greenhouse gas emissions faster.

The steel sector can play a key role in this. Often labeled as a hard-to-abate sector, the steel sector has the potential to turn into a fast-to-abate sector: our study demonstrates that a net-zero iron and steel sector by the early 2040s is technically feasible.

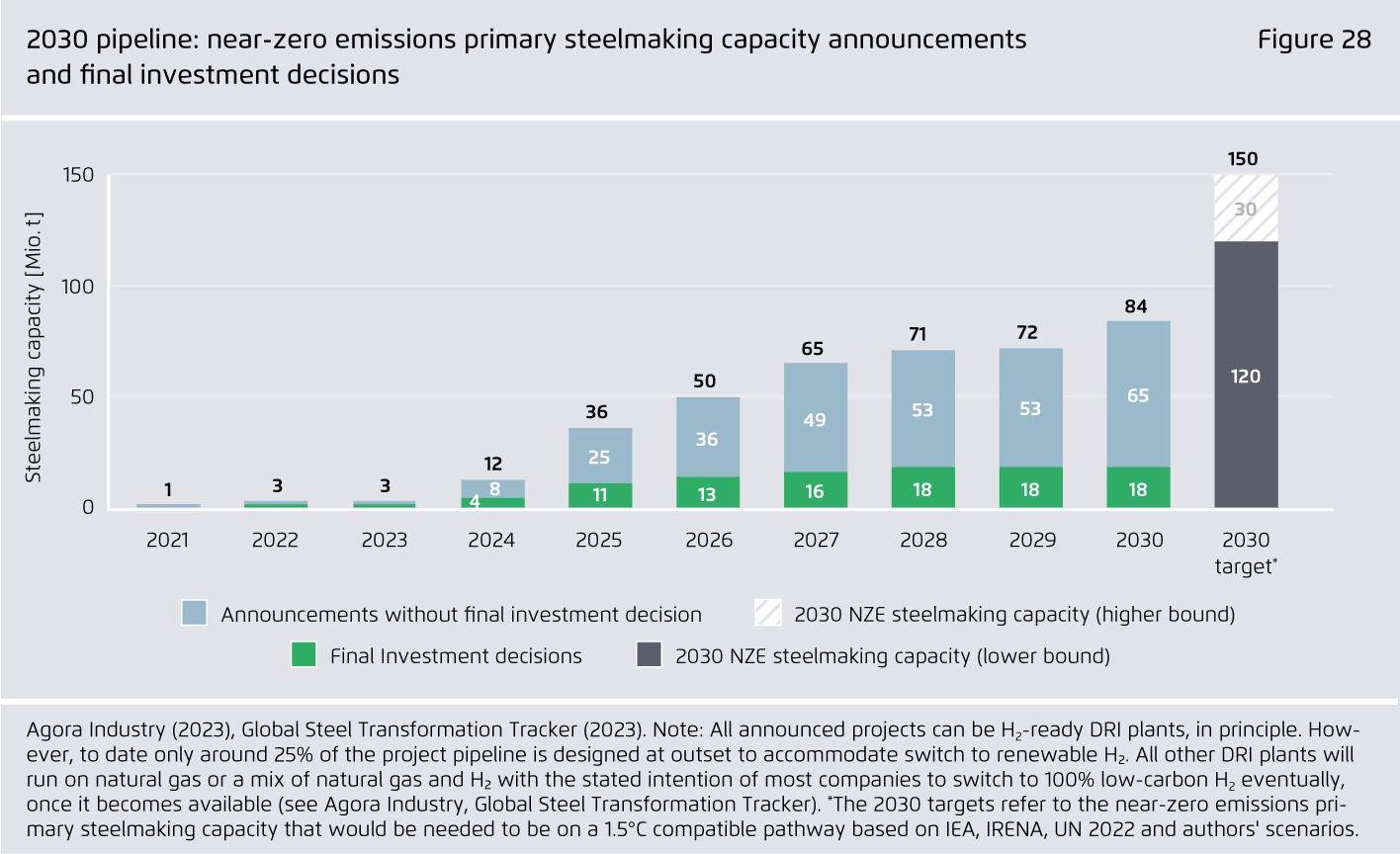

New key elements for an accelerated, lower-cost steel transformation include a swift roll-out of direct reduced iron technology, the creation of an international green iron trade, the phase-out of coal in steelmaking, and, above all, expanded international cooperation in tandem with targeted regulatory frameworks.

This study summarises the key findings of our work on the global steel sector. In future publications, we will provide more detailed analyses of low-carbon technologies, our 2050 decarbonisation pathways, the role of international green iron trade and the steel sector’s potential to generate negative emissions.

Key findings

Bibliographical data

Downloads

-

Impulse

pdf 5 MB

15 Insights on the Global Steel Transformation

This study summarises the key findings of our work on the global steel sector.

-

議論への一石

pdf 6 MB

世界の鉄鋼産業の 脱炭素化に関する 15の知見

Impulse in Japanese

-

Impulse

pdf 5 MB

15 Wawasan tentang Transformasi Industri Baja Global

Impulse in Indonesian

All figures in this publication

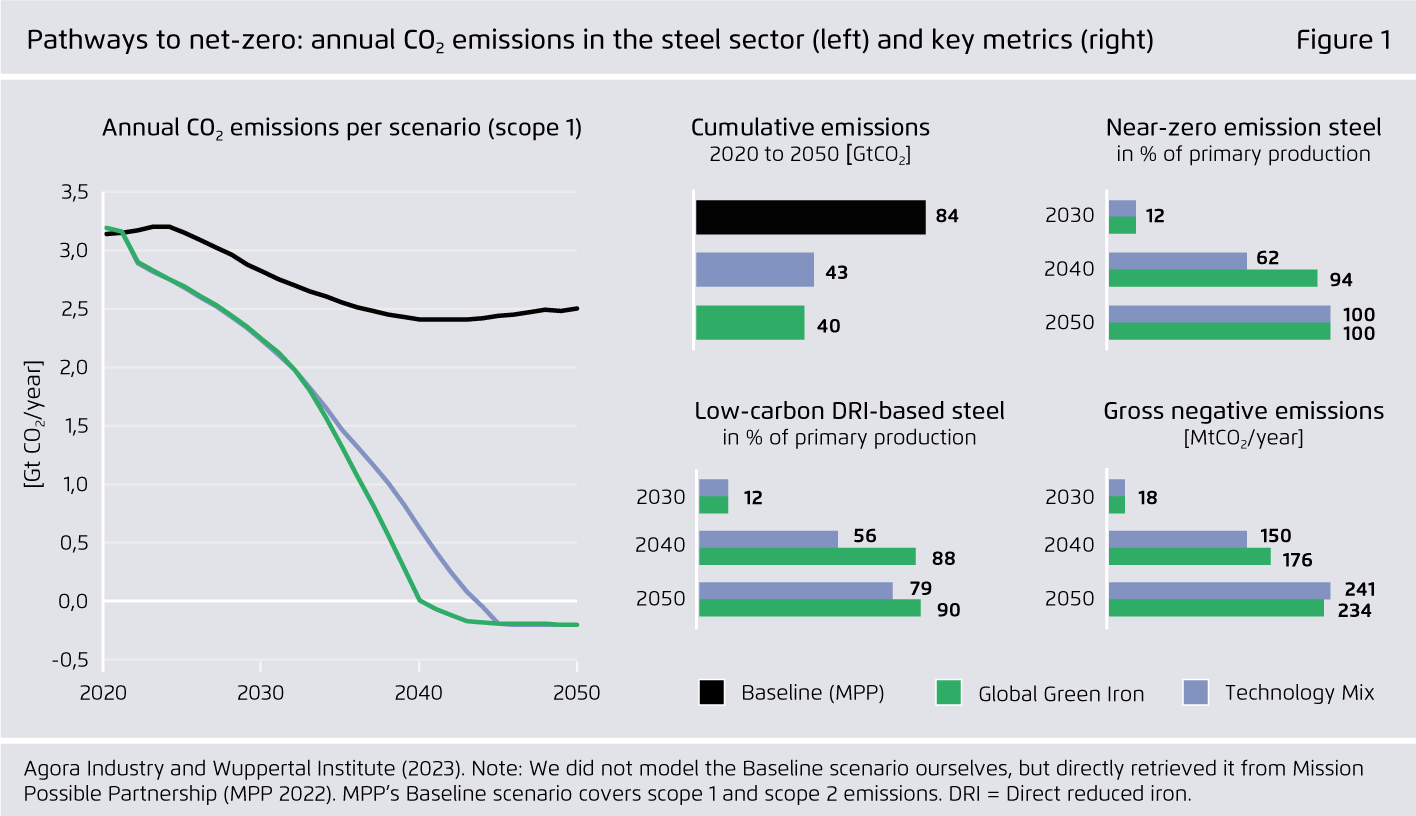

Pathways to net-zero: annual CO₂ emissions in the steel sector (left) and key metrics (right)

Figure 1 from 15 insights on the global steel transformation on page 8

Share:

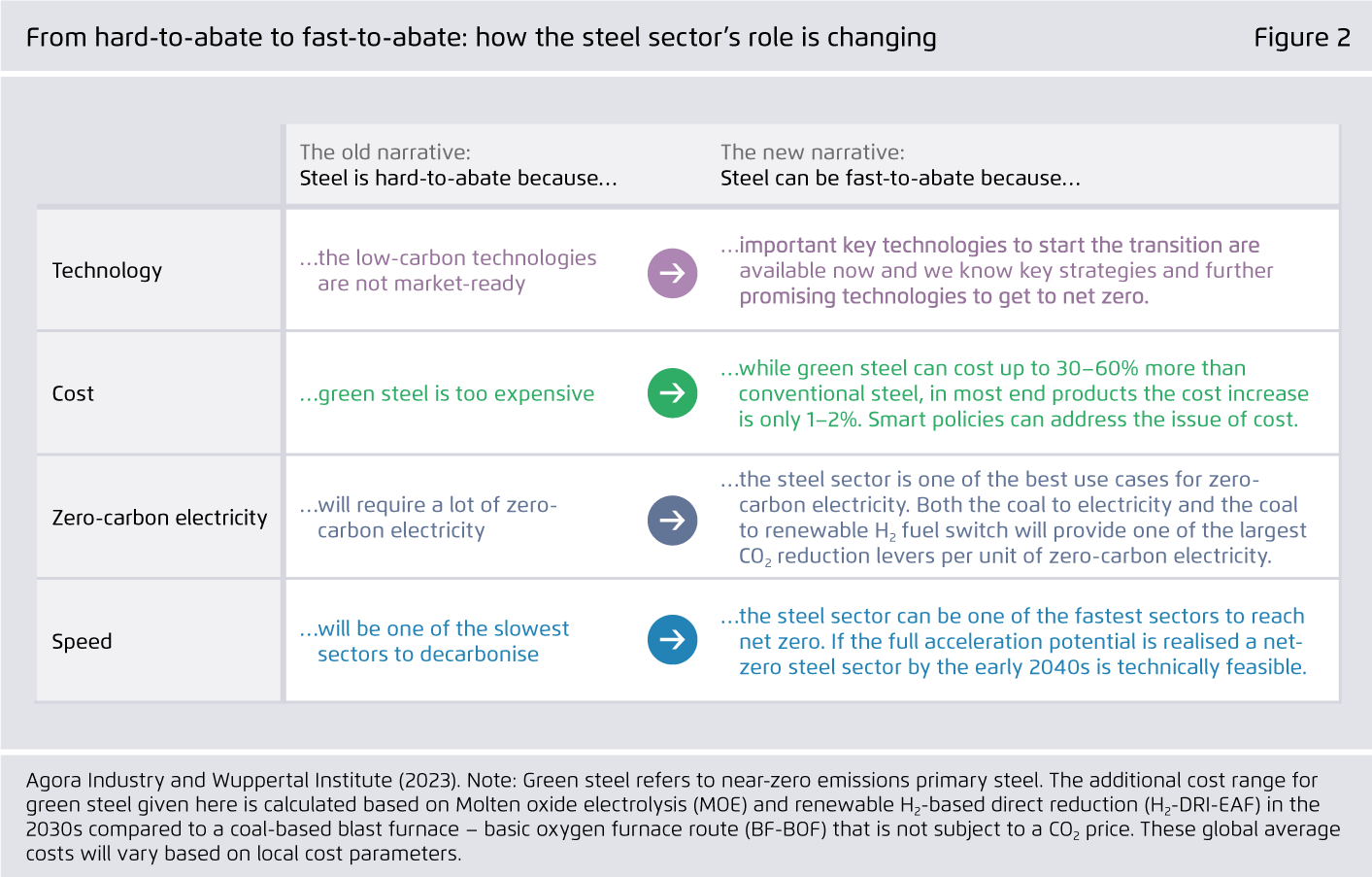

From hard-to-abate to fast-to-abate: how the steel sector’s role is changing

Figure 2 from 15 insights on the global steel transformation on page 9

Share:

Our experts

-

Wido K. Witecka

Project Manager Industry (until June 2024)

![[Translate to English:]](/fileadmin/_processed_/8/f/csm_15_insights_global_steel_news_73f640a802.jpg "The global steel industry can achieve net-zero emissions by the early 2040s")

![[Translate to English:]](/fileadmin/_processed_/9/e/csm_global-steel_project_news_2_283e600f74.jpg "Shifting global steel reinvestments from coal to clean")